Whenever you make money at anything, including gambling, you always have to worry about the tax man. (Photo credit: Alan Cleaver via Foter.com / CC BY)

Just as there are misconceptions about the legality of sports betting in Canada, there is also a lot of confusion about another question: Are gambling winnings taxable in Canada?

It’s always difficult to find definitive answers to these types of legal questions, since no one wants to open themselves up to potential liability for giving out some bad advice.

So we decided to do something about it. We’ve done a lot of research on the subject and reviewed analysis by experts in both the legal and tax industry.

And we’ve concluded that if you’re like 99.9% of sports bettors – working full-time and betting sports on the side – you’ve got nothing to worry about when it comes to paying tax on gambling winnings, Canada residents particularly.

Good news There is no income tax in Canada on gambling winnings. https://t.co/SDwSHwrJtU

— Robert Raiola, CPA (@SportsTaxMan) September 25, 2015

Not just that, but even if you bet on sports full time and were able to make a living off it, there’s still a very strong chance you’d never have to pay income tax on your winnings.

The big reason is that it’s nearly impossible to define the difference between someone who bets for fun and someone who bets as a business. Both are pursuing profit, both can be spending dozens of hours per week doing it, both can have ‘systems’ that analyze and minimize risk, etc.

Basically, if the government were to collect income tax from winning sports bettors they claimed were professional, they’d also be opening themselves up to having losing “professional” bettors claim their losses as tax deductions.

“There is no tax on a habit”

Before we get into the legal history of taxation of gambling winnings in Canada, we need to go back to a 1928 case in England when the British government attempted to force a successful horse bettor to pay income tax on his winnings.

Highly-respected English tax judge Rowlatt J. sided with the bettor, noting the bettor may have been skilled but that there was no way to conclude that gambling was his job.

“It seems to me that people would say he is addicted to betting, and could not say that his vocation is betting,” the judge said. “There is no tax on a habit.”

Though this ruling was made nearly 100 years ago and in another country, it has had a significant impact on how our legal system views the concept of sports betting income tax in Canada.

Other court cases impacting gambling winnings tax in Canada

Much of our legal system is based on precedent, also known as case law. When deliberating a case, judges research how similar cases were ruled in the past and typically make their ruling based on that.

Here is a quick summary of two other major precedents that impacted the issue of sports betting income tax in Canada:

- Moldowan v The Queen (1978): Moldowan, an otherwise-successful businessman, attempted to claim significant losses from his horse-racing farm as deductions on his income tax. He argued that his farm was a source of income and that he should be entitled to claim losses as a deduction. The Supreme Court of Canada ruled that his horse-racing business had no “reasonable expectation of profit” and that it wasn’t a primary source of income for him, and limited his deductions at $5,000 per year.

- Stewart v Canada (2002): Stewart, a savvy real-estate investor, attempted to write off $57,000 of interest expenses he was charged for borrowing money to purchase four rental units near Ottawa in 1986. The Canadian Revenue Agency had denied those deductions because they believed his business had no ‘reasonable expectation of profit’, which was the precedent set in Moldowan v The Queen. However, the Supreme Court of Canada determined the concept of ‘reasonable expectation of profit’ was vague and uncertain, and instead ruled that Stewart was entitled to claim the losses because he was “in the pursuit of profit.”

Are Gambling Winnings Taxable in Canada – What the law says

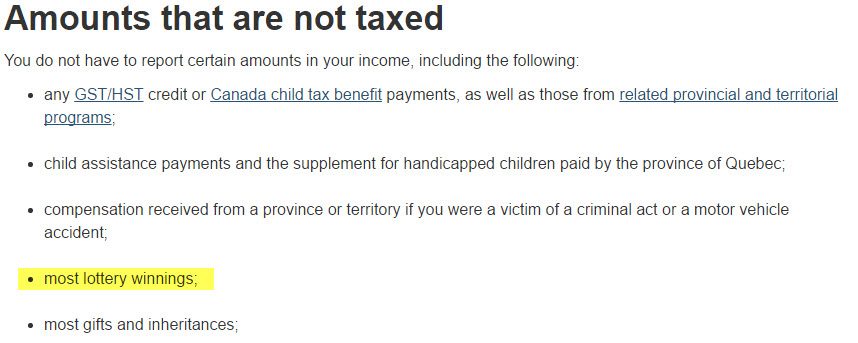

On the Canadian Revenue Agency (CRA) website, there is a page that lists the types of income that you do not need to declare on your tax return.

Included in that list is “most lottery winnings.” That’s because occasional lottery winnings in Canada are considered a windfall, according to the Canada Income Tax Act.

However, sports betting winnings are a lot more than occasional. If you regularly bet on sports, you’d probably win several bets per day on average – although those winnings will be a lot less than the millions of dollars you could collect winning Lotto 6/49.

So what does the law say about that? Well, the CRA website also covers gambling profits extensively in a section that explains tax liability on non-traditional income sources.

In that section, the CRA states that “an individual’s gambling activities may result in taxable business income or a business loss. This will be the case if the gambling activities constitute a source of income (that is, carrying on the business of gambling)”

But the CRA is also quick to admit that “determining the commerciality of gambling can be challenging.” That’s because what ordinarily may be viewed as a business are also common practice for anyone who gambles.

After all, no one walks into a casino or places a sports bet hoping to lose.

We’re all trying to make money at it, even if the odds are against us. We can have systems (whether they be any of the popular sports betting money management systems, or handicapping systems we use to pick more winners), and we can spend a lot of time on it. We can even read lots of strategy books or articles in the hopes of improving our skills.

That doesn’t make us professional gamblers, and it doesn’t make our sports betting a business – even if we’re profitable.

And the courts have agreed with us in the past.

Cases When Winning Gamblers Have Not Had To Pay Tax In Canada

Leblanc Brothers

The most prominent court case regarding tax on gambling winnings in Canada involved two Ottawa-area brothers, Brian and Terry Leblanc, in 2006.

The Leblancs had averaged earnings of $650,000 per year from 1996-99 playing sports lotteries in Ontario and Quebec. The Canadian Revenue Agency insisted the Leblancs had to pay tax on their winnings because they ran their operation as a business.

The CRA’s argument was based on the following points:

- The Leblancs bet $10-13 million per year

- They wrote computer programs to analyze bets

- They negotiated 2-3% ticket discounts from retailers

- They had hired up to 15 people to help buy their tickets

- They managed and organized their efforts in the pursuit of profit

- Their lone source of income was their gambling winnings

However, the Tax Court of Canada ruled in favour of the Leblancs, noting how it is rare to consider gambling as a business and instead referring to it as a “personal endeavour.”

The Leblanc case is widely considered to be a landmark decision against taxing gambling winnings in Canada because the CRA’s case was so strong. By winning so much money over such a long period of time, the Leblanc brothers clearly had devised a system to beat the provincial sports lotteries, but the judge still ruled they were “compulsive gamblers… continually trying their luck at a game of chance.”

“It has arguably never been clearer that the courts will not be inclined to consider gambling gains to be income from a business,” Benjamin Alarie, a University of Toronto law professor and the CEO of Blue J Legal, wrote for the Canadian Tax Journal in 2011, “in the absence of a proven system for profit making (such as a bookmaker or an operator of slot machines or VLTs), clear evidence of inside information (such as receiving tips on horses), or other means of ensuring success (for example, cheating at online poker through various reliable, though illicit, strategies, such as conspiring with others at the same table.”

Poker Player Peter Radonjic

More recently, there was a fascinating case in 2013 involving Peter Radonjic, an online poker player from Coquitlam, B.C.

What made Radonjic’s case so compelling was that he had actually paid taxes on his online poker winnings from 2004-07, feeling it was better to be safe than sorry and that he would be refunded the money if his earnings weren’t found to be taxable. Radonjic had quit doing contract work for the government in 2004 in order to focus on playing online poker, and had been led to believe that he needed to report his poker winnings since they were his primary source of income.

After speaking to several fellow online poker players, however, Radonjic realized his winnings might not have been taxable after all. He filed adjustments to the CRA for the four years he paid taxes on his poker winnings, but the CRA denied his claim on the basis that Radonjic was a professional poker player.

Radonjic eventually took his case to court, arguing that he was being punished for being a responsible citizen and having faith in the system, and that the house (online poker sites) are the only party in online poker who has a reasonable expectation of profit. He also noted that past precedent in Canadian law supported his case, including the Leblanc verdict.

The Canadian Federal Court sided with Radonjic, and listed the following reasons for its decision:

- Just because Radonjic made money did not mean he had a realistic expectation of profit, or that he had a system

- Any poker player wants to win money and narrow the odds in their favour

- Cutting back on other work and income is no indicator of running a gambling business

“The luxury of being able to work less is one of the fruits of successful gambling, just as having to work more may be one of the results of unsuccessful gambling. Chance dictates the outcome in either case,” the judge ruled.

According to Alarie, who discussed the case in a University of Toronto Faculty of Law blog post, the Radonjic case shows how difficult it is for Canadian government to label any gambler – regardless of their success – as a professional.

“Prior to Radonjic, it was clear that there is a strong legal presumption that gambling winnings and losses are beyond the reach of the Canadian income tax. This presumption now appears to be stronger in the aftermath of Radonjic,” Alarie wrote.

“The challenge for the government relates to showing that an individual poker player is carrying on the business of playing poker professionally when the Minister cannot validly rely on the player’s winning record, the player’s intense play over a long period of time, the player’s attempts to improve, the player’s reliance on gambling for a livelihood, or the player’s keeping (or not keeping) of records.”

Losing Gamblers Have Been Denied Claiming Losses As Tax Deductions

Labelling gamblers as ‘professionals’ in order to tax their income is a double-edged sword for the Canadian Revenue Agency.

For every successful sports bettor, there is a hundred losing ones. If winning gamblers are required to pay taxes on their net income, losing gamblers would need to be able to claim their net losses as tax deductions.

In fact, several have tried. And they haven’t fared very well in tax court.

Here’s a look at three of the higher-profile cases:

- Molony vs Minister of National Revenue (1990): Molony embezzled more than 10 million dollars from his employer, the Canadian Imperial Bank of Commerce, to fund his gambling addiction, losing it all. In his tax returns from 1980-82, Molony claimed the embezzled money as income, and also included his gambling losses as deductions. The Tax Court of Canada ruled the deductions were not permissible because Molony was not a professional gambler. “It is self-contradictory to speak of a pathological gambler being in the business of gambling,” the judge said. “This activity impairs his intellect and his sense of perspective is lost. The impulse to go on regardless of the financial consequences is overwhelming. His attitude is irrational.”

(Molony’s story was the inspiration for the 2003 movie Owning Mahowny, starring Philip Seymour Hoffman and Minnie Driver.)

- Cohen v The Queen (2011): Cohen was a Toronto-based lawyer who decided to leave his high-paying job in 2006 to become a professional poker player. He read numerous books, attended seminars, studied for hundreds of hours and played poker 8 hours a day, but he lost $122,000 in his first year. When Cohen attempted to claim his losses as a tax deduction, the CRA denied the claim on the basis that poker was Cohen’s hobby, not a business. The Tax Court of Canada agreed, ruling that buying books and attending seminars did not equal business training, that Cohen did not have a legitimate business plan, and that he did not have a reasonable expectation of profit.

http://bit.ly/lR0hpH Again, the Canadian courts have shown their reluctance to tax #poker winnings & allow deduction of poker losses.

— Stuart Hoegner (@GamingCounsel) June 16, 2011

- Tarascio v Canada (2012): Tarascio, who worked full-time as a Bell Canada technician, lost approximately $100,000 on gambling from 2002-03. He kept detailed records of his wins and losses during that time, and argued that his gambling experience and his degree in mathematics gave him the skill to be a professional gambler. The Minister of National Revenue disallowed Tarascio’s attempt to claim his losses as tax deduction, however, on the basis that Tarascio’s gambling was not a business. The Federal Court of Appeal supported the Tax Court of Canada’s ruling that Tarascio was not entitled to claim losses, stating that keeping detailed records did not make him a business, that he played for enjoyment, and that he did not have a systematic method for winning.

In all three cases, the prevailing reason why the gamblers were denied in their attempt to claim their losses as tax deductions was because the court ruled they had no realistic expectation of profit.

In his 2011 article for the Canadian Tax Journal, Alarie wrote the only way courts would consider someone to be in the business of gambling is if they are “actually in a position to ensure that gambling will provide consistent and reliable profits through, for example, providing gambling opportunities to others, relying on inside information (as an informational entrepreneur), or deploying considerable skill, knowledge, and expertise to tilt the odds in his or her favour.”

Cases When Someone In Canada Had To Pay Tax On Gambling Winnings

There has been just a few instances in Canadian history when winning gamblers were required to pay tax on their earnings.

In almost all of them, the reason the gambling winnings taxable in Canada verdict was reached was because those winnings were related to his profession.

Here are three examples:

- Dowling v The Queen (1996): Dowling was a golf pro who often also gambled on his golf games, poker games and sporting events. The Tax Court of Canada ruled that Dowling did not have to pay tax on his earnings in poker and sports betting, but that he did have to pay tax on earnings from gambling on his own golf games (which was approximately $5,000 per summer). The reason Dowling was liable for tax on his golf betting was because he was a professional golfer who was better than his amateur opponents and could “reasonably have expected to win about 90 per cent of the games he played.” He was not held responsible for earnings from other gambling because he did not have a similar edge or expectation of profit.

- Badame vs MNR (1954): Badame raised and raced as many as 18 horses for a living. He also routinely bet on horse racing (both his own horses and others’ horses), spent almost all of his time at race tracks and earned more than $13,000 betting horses from 1947-48. The judge determined his horse-betting winnings were part of his business because Badame had special access to race tracks; closer association with owners, trainers and jockeys; and could do checkups on horses before races – all of which diminished his risk.

- MNR v Walker (1952): Walker was a horse-racing bettor who owned or had other interests in several horses. For a decade, he systematically attended races in four different cities and profitably bet on most of them. He was ruled to be in the ‘business of gambling’ because he had the benefit of inside information from jockies and “other interested persons on the probable outcome of races,” which made him much more likely to win than the average bettor.

According to Canadian gaming lawyer Jack Tadman, there is only one case in Canadian law where someone had to pay taxes on gambling winnings that had no connection to a previous business or occupation.

That case was Luprypa v. Canada (1997), which involved a man who had lost his job and began playing pool for money at a local bar. Over a span of nearly one year, he won approximately $1,000 per week by playing late at night Monday to Friday against drunk opponents.

It was determined that Luprypa had to pay tax on those winnings because he was a professional gambler, not a recreational one.

The court highlighted these points about Luprypa when labelling him as a professional:

- He carefully managed his risk

- He was skilled

- He played every week from Monday to Friday

- He practiced every afternoon to develop his skills

- He minimized his risk by only playing drunken opponents after 11 p.m.

- He won money the majority of the time, averaging $200 per day

- He only drank on weekends, remaining sober during the week to take advantage of his opponents

- He was calculated and disciplined in his gambling

- He relied on gambling on pool as his primary source of income

“(The judge) held that where a person uses expertise and skill to earn a livelihood in a gambling game in which skill is a significant component, their gambling winnings are taxable,” Tadman wrote in a 2009 article for Canadian Gaming Lawyer Magazine.

“The rule in Luprypa is limited to gambling games where skill is a significant component. How does one determine whether the skill required to excel at a gambling game is ‘significant’ enough for the rule in Luprypa to apply?”

Are gambling winnings taxable in Canada? The last word…

In order for you to be charged income tax on gambling winnings in Canada, it must be proven by the government that you are in the “business of gambling.”

That is an incredibly difficult thing for the government to do.

The courts have shown repeatedly that just because you are a successful, profitable gambler does not mean that gambling is your business. They have also shown that the amount of time you spend gambling, whether you have any other sources of income, how organized and systematic you are, or how educated you are about gambling does not make you a professional gambler.

Based on legal precedent, it appears the only ways you will be ruled to be in the business of gambling is if the gambling is directly related to your profession or business, if you have access to inside information that greatly increases your expectation of profit, or if you possess tremendous skill that gives you an insurmountable advantage over your opponents.

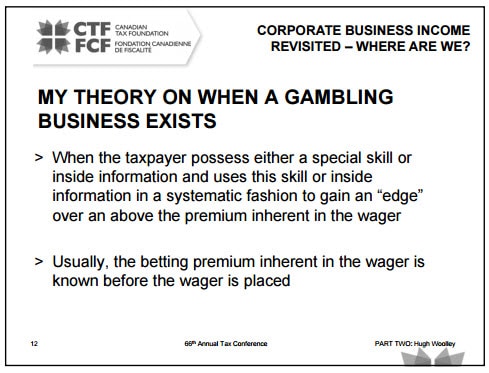

In a 2014 presentation at the Canadian Tax Foundation’s 66th annual tax conference in Vancouver, Ian Gamble of Thorsteinssons LLP included this slide.

For the average sports bettor who has to win 52.38% of his bets against the point spread to simply break even, none of these conditions seem applicable.

“Rooted in the British common law, and codified by paragraph 40(2) (f ) of the Income Tax Act, Canada has a longstanding tradition of not taxing gambling winnings,” Tadman wrote in 2009.

“Unless the gambling winnings of the (gambler) are directly related to their vocation, or they are skilled pool or card players preying on unsuspecting marks, the money they win will be (almost) twice as sweet as the money they earn.”